Smart Cap – Good for the State, Good for the County

Posted by PBCTAB on April 28, 2011 · Leave a Comment

The Florida Legislature is moving forward on a constitutional amendment for the 2012 ballot to limit state spending to a “growth factor” tied to inflation and population growth. A previous attempt in 2009 had included county and municpal governments in its scope, but that has been omitted this time.

We think it is still a good idea however, and could be implemented for Palm Beach County as a Charter Amendment. TAB plans to argue both for and against the various proposals coming forward during the charter review process. Since a Smart Cap is not likely to be proposed by the Board themselves, we want to raise this proposal now so it can be discussed and perhaps gather momentum.

This article examines the effect a smart cap would have had on the county if it were in place since 2003. The conclusions are:

- The FY2011 ad-valorem equivalent for the county-wide departments is 15% less than a cap would have allowed. This is good and reasonable. It was achieved however, by significant reductions over the last three budget cycles, coming off a peak in 2008 that was 7% over cap, and a record of exceeding the cap in all but the last two years.

- It would have greatly restrained the growth in PBSO and Fire/Rescue, as their FY2011 ad-valorem equivalent exceeds what the cap would have allowed by 32% and 19% respectively. Since both of those organization’s budgets are primarily personal service costs, the existence of a cap would have limited the salary and benefit enhancements that were granted in the lucrative collective bargaining agreements that are now such a drag on the county budget.

- If a cap were to be imposed, it could be crafted in such a way that emergency overrides are possible.

- Although we are not enthusiastic about the overuse of federal grants for local projects, a county “Smart Cap” would not interfere with the use of such funds.

- There is precedent – both Duval and Brevard counties (and possibly others) have caps in place today.

For these reasons, we would very much like to see a county version of Smart Cap on the 2012 budget as a result of the Charter Review.

What is Smart Cap?

Senate Joint Resolution 958, introduced by Senator Ellyn Bogdanoff and approved by the Florida Senate on March 15, would place a constitutional amendment on the 2012 ballot to limit the growth in spending at the state level. House Joint Resolution 7221, an identical bill, has passed out of committee and is pending a floor vote.

Unlike a previous attempt at a Florida “Smart Cap” (SJR1906), introduced by now Senate President Mike Haridopolis in 2009 and applying to county and municipal governments as well, the current iteration would apply only to the state budget. It’s provisions (summarized in the staff analysis) are:

- Replaces the existing state revenue limitation based on Florida personal income growth with a new state revenue limitation based on changes in population and inflation

- Requires excess revenues to be deposited into the Budget Stabilization Fund, used to support public education, or returned to the taxpayers

- Adds fines and revenues used to pay debt service on bonds issued after July 1, 2012 to the state revenues subject to the limitation

- Authorizes the Legislature to increase the revenue limitation by a supermajority vote

- Authorizes the Legislature to place a proposed increase before the voters, requiring approval by 60 percent of the voters

It should be noted that the “revenue” that is capped is subject to some exclusions. It does not apply to Medicaid funds, revenue necessary to meet bond requirements, federal grants and some other revenues. The amendment would replace the current cap which is based on personal income. Currently, 32 states have some kind of statutory cap on spending.

Palm Beach County Smart Cap

On the county level, a “Smart Cap” could be instituted through a Charter Change amendment on the 2012 ballot. Would this have much effect on the budget?

TAB has pointed out that the county budget overall has grown “11 times population growth and 3 times the rate of inflation” from $1.2B in 2003 to $2.1B in 2011. This tracks spending growth though, and is partly funded by revenue that under the state rules would be exempt such as federal grants. It also includes “fee for service” revenue that varies with the services requested, and other revenue that is department specific. For simplicity, we have chosen to look at the effects of a “Smart Cap” by analysing the “ad-valorem equivalent” amount at the department level. This number is the difference between the spending proposed by a department (appropriations), and the revenue it receives from specific sources like grants or fees, and is paid for by a combination of ad-valorem taxes and other “ad-valorem equivalent” revenues such as the sales tax.

The revenue cap at the state level is based on a “population and inflation” model, and sets the cap at last year’s revenue limit plus a growth factor. The growth factor is computed by combining inflation represented by the consumer price index (CPI) and the state population as used in other measures. In other states, most notably Colorado’s “TABOR”, the Taxpayer Bill of Rights, the cap was applied to the previous year’s revenue. Since revenue declines during a recession, this caused the cap to “ratchet” down and caused more spending reduction than was anticipated or desired. It was suspended for a period of time by the legislature to allow the economy to equilibrate. The Florida proposal does not have this problem since the growth factor is applied to the previous year’s cap – not the revenue collected (after a multi-year startup phase).

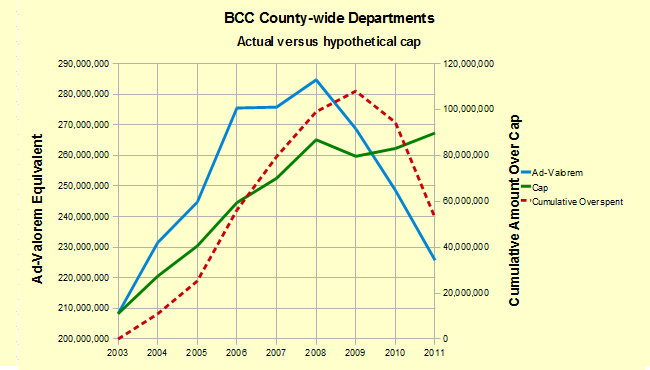

To see the effect had Smart Cap been in effect in 2003, we can compute the growth factor from that year’s budget forward to 2011, and compare it to the actual budget growth that occurred. The results show that while PBSO, Fire/Rescue, and the Supervisor of Elections all grew much faster than a cap would have allowed, the countywide departments are now comfortably 15% under what the cap would require. Bob Weisman has always maintained that his growth was “less than TABOR”, – and it was, if you only look at the endpoints. You just have to separate his budget from the others to see it clearly. The 8 year trend is shown in the following chart. Unfortunately, the overspending in the early years resulted in a cumulative overspend of about $50M.

County-wide Departments ad-valorem equivalent compared to a “smart cap”

The following table illustrates what the FY2011 budget (ad-valorem equivalent) would have been had Smart Cap been in place since 2003. The “Growth Factor” is computed by combining the change in CPI and the change in service population for the period 2003-2011, and is 28.4% countywide. Fire / Rescue has expanded their service area during the period from 641,000 to 807,727 by taking over municipal departments, so their growth factor of 52.5% reflects that change. Likewise, the Library system has grown their population by about 13% during the period, now providing service to 28 of the 38 municipalities for a growth factor of 37.2%.

The Sheriff has also grown the PBSO service area during the period by taking over law enforcement duties in Pahokee, South Bay, Belle Glade, Royal Palm Beach, Wellington, Lake Worth, Mangonia Park and Loxahatchee Groves. We did not adjust the PBSO growth factor however, because unlike Fire/Rescue, they are funded from county-wide ad-valorem taxes and the change in service area is offset by specific contract revenue from the towns and cities that have been absorbed. Corrections, court protection and law enforcement infrastructure (crime lab, SWAT, etc.) are funded by all county taxpayers.

| 2003 Ad-valorem Equivalent | Growth Factor | 2011 Cap | 2011 Ad-valorem Equivalent | Exceeded Cap By | |

|---|---|---|---|---|---|

| County-Wide Departments | $208M | 28.4% | $267M | $226M | -15.4% |

| Fire / Rescue | $113M | 52.5% | $172M | $205M | 19.2% |

| Library System | $26M | 37.2% | $36M | $38M | 6.4% |

| Constitutional Officers | |||||

| Sheriff | $236M | 28.4% | $303M | $400M | 32.0% |

| Clerk * | $31M | 28.4% | $39M | $12M | -69.2% |

| Property Appraiser | $14M | 28.4% | $18M | $18M | 0.0% |

| Supervisor of Elections | $5M | 28.4% | $6M | $11M | 83.3% |

| Tax Collector | $4M | 28.4% | $5M | $4M | -20.0% |

Note: The large reduction in the Clerk’s budget is a result of conversion of some ad-valorem items to a fee basis in 2005.

The eight year growth in spending has shown that portions of the county, including the county-wide departments and the constitutional officers (except the Sheriff and SOE) have been responsible in adjusting their budget appropriate to the size of the county population and consistent with price inflation. It should be noted however, that until the valuations began to decline after 2008 there was not much evidence of restraint.

We will examine the relationship of spending to the cap on a year by year basis in an upcoming article.

PBSO and Fire/Rescue on the other hand have grown way out of proportion, and most of the increase has gone into salaries and benefits for those covered under collective bargaining agreements. It is time to rein this in, and a Smart Cap Charter amendment is a way to do it.

Put Smart Cap on the ballot in 2012 and let the people decide.