Try out our NEW interactive District Map

Ever wonder to what distirict a particular neighborhood or street belongs? The county website maps can help, but they don’t show all streets. TAB now provides a fully interactive Google Map of the county, that shows the district lines, and may be zoomed in or out. Clicking on a location brings up a box with the commissioner and their phone number.

Try it out here, or find it under the TAB “Resources” tab.

View bcc in a larger map

County Commission Holds Off-Site Retreat

At Newcomb Hall in the Riviera Beach Marina today, County Commissioners sat in an open circle with Administrator Bob Weisman and County Attorney Denise Neiman. In this casual setting, they got to know each other better, discussed priorities for the next 5 years in the morning, and previewed the coming budget in the afternoon.

Each commissioner had their own priorities to discuss, but some common themes were “sustainability” – preparing for higher energy and water costs and their implications to the county, Everglades restoration, dealing with the problems in the Glades communities, and building on the investments already made in Biotech.

The budget discussion was a preview of what is to come, somewhat suggestive of the narrative during last September’s hearing. With the Property Appraiser projecting a 5-8% decline in values for the next tax year, the initial county planning number is 5% (6% decline in current property with 1% new construction according to Budget Director Wilson). This puts the estimated valuation at about $121B.

In order to have the same countywide ad-valorem tax revenue as 2011 ($603M), a millage increase to over 5.00 would be required. Since 5 is a “psychological barrier”, Adminstrator Weisman projected that 4.95 would be his recommendation to avoid significant cuts. The commissioners on the other hand, were more of a mind to hold the millage flat at 4.75 and asked for a budget at that level with a list of the cuts necessary to achieve it. Commissioners Burdick and Marcus reported feedback from constituents that they would rather see cuts in services than tax increases. Commissioner Aaronson on the other hand says his folks don’t mind paying more to keep the services they have come to expect. In any case, there was consensus for the 4.75 sizing and that is what will be returned. Since the Sheriff’s budget is about half of the countywide ad-valorem, he has been informed that flat millage will require $25M from his budget.

(TAB comment: It should be noted that flat millage with a 5% reduction in valuation from $127B yields a $30M shortfall. Additional reductions in other revenue sources are expected though – from the gas tax and federal grants among others. Therefore, the problem will likely be more like $50-60M at least).

For media accounts of the meeting, CLICK HERE for the Sun-Sentinel, and HERE for the PB Post.

Palm Beach County Pay and Benefits – How Much is Enough?

There is much anecdotal evidence, both locally and nationally, that public sector compensation has far outpaced that in the private sector. During this prolonged period of economic downturn, there is a perception that while many are out of work, underemployed, or making do with reduced pay and benefits, the public employee gravy train just keeps rolling along.

Editor’s Note

Prior to publication, this study was sent to Fire/Rescue, PBSO, and county staff for comment. Feedback from county staff suggested our pension comparison, while numerically accurate, was artificial since few special risk employees stay for 30 years – most retire at 25. The Sheriff did not comment but we will add his remarks if he does so at a later date.

Fire Chief Steve Jerauld did not dispute the numbers, but thought the comparison to PBSO was not “apples to apples”, since the Sheriff employs a large number of non-sworn civilian employees. He also explained that the apparent overabundance of supervisory titles relates to how they deploy their equipment. Each Engine deploys with a captain, and each Rescue unit with a lieutenant.

Given these points, we added a section to the study that directly compares the sworn titles in Fire/Rescue to those in PBSO. Under those assumptions the difference is not so stark, but the salaries in F/R are still 5-7% higher than in PBSO, on average.

We have attached Chief Jerauld’s comments in their entirety at the end of the article. Click HERE.

But is this really true in Palm Beach County? Many would say it is not – that wages have been frozen, and the compensation provided is really much less than has been claimed. TAB decided to dig into the numbers and see for ourselves.

The results may surprise you, but we found the gross pay for PBSO rank and file (total organization, sworn and unsworn, not management) and county staff to be within range of both local and national averages provided by the Bureau of Labor Statistics. Fire/Rescue on the other hand, seems to have won the public sector pay lottery, coming in over 50% above their peers nationally. When measured in terms of just sworn positions, PBSO staff and management do see a 29% premium over the national average, and a slight advantage over their local peers in the West Palm – Boca corridor.

Pension benefits are a different matter. As Defined Benefit plans go, payouts for those in the “regular class” FRS plans are good but not excessive. Of course just having a DB plan is generous – only 21% of private sector jobs are so blessed, according to the Cato Institute. For those in “special risk classes” like sworn positions in both Fire-Rescue and PBSO, the pensions are extremely generous. In a future article, we will explore the funding assumptions behind these pensions, and see what they suggest about future financial risks for the county.

Source Materials

The conclusions we draw in this study are only as good as the source materials. We do not work in county Human Resources, and have no insider knowledge. Rather, we are using publicly available source materials, and extrapolate from those when necessary to align to subject years. The sources used are:

- County Budget Books for years 2004-2011 (“Fiscal Year 20xx Annual Budget)

- Budget detail from PBSO obtained through Chapter 119 Open Records Requests.

- Salary, Overtime, Title, Department data for each employee, maintained online by the Sun Sentinel (2009 data).

- Florida Retirement System plan descriptions

- Miscellaneous data from County, PBSO, Fire-Rescue, and IAFF websites

- Mean salary data from the Bureau of Labor Statistics

For comparisons, total compensation is based on the 2011 budget. Direct measures of gross pay are based on 2009 data in the Sun-Sentinel database and the 2009 BLS study.

Measuring Compensation

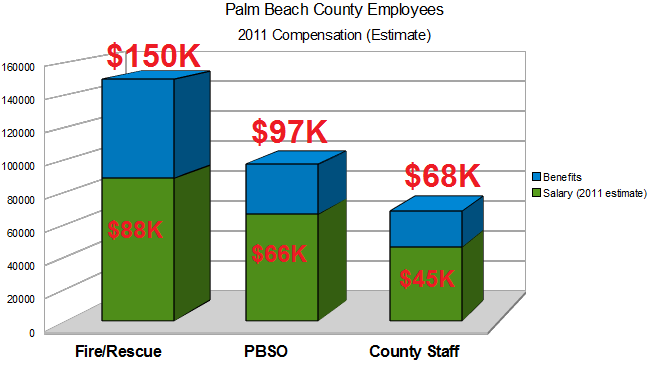

For the sake of the comparison, we divided the 11,166 county employees into the three major areas that stand alone by nature of their mission and bargaining units. These are the Sheriff’s office, County Fire/Rescue (which has its own MSTU), and the rest of the staff, including those reporting to Administrator Weisman as well as those who work for the Constitutional officers exclusive of PBSO.

| Area | Employees | Personal Services Budget | % of Total | Per Employee Average |

|---|---|---|---|---|

| PBSO | 3,919 | $390M | 39% | $97,233 |

| Fire-Rescue | 1,511 | $226M | 22% | $149,570 |

| County Staff | 5,736 | $389M | 39% | $67,876 |

| Total | 11,136 | $1,005M | 100% | $90,248 |

The County Budget Book defines “Personal Services” expense as “Items of expenditures in the operating budget for salaries and wages paid for services performed by county employees; including fringe benefit costs.” This is also known as “compensation”, and includes:

- Salary

- Overtime

- Special pay and bonus

- Pension contribution

- Health insurance

- life insurance

- FICA payments on behalf of the employee

These compensation costs are what an employee “earns”, or put another way, the variable cost to the county for employing the individual.

In order to compare these numbers to the private sector (or in the case of Fire and PBSO, peer agencies here and elsewhere), we would need to separate out the “pay” component from the “benefit” component, particularly since many articles written on the subject claim that it is the benefits that really separate government employees from their counterparts in the private sector. Luckily, a snapshot of what each employee was paid in 2009 was obtained by the Sun-Sentinel and made available to the public. The database provides the employees name, title, department, salary, and overtime. PBSO is in one database, and the rest is in a second, but Fire/Rescue is easily separated from county staff using the department field.

With a little programming and the magic of SQL, this data was used to extract average salary data for the three groups, and later to refine it into separate averages for “management” and “staff”. The 2011 equivalent was then obtained by advancing the Fire-Rescue average using the contracted raise amount from the collective bargaining agreement, and using a figure of 2.5% for the other groups. Combined with the “compensation” data, the result is the following chart:

We were surprised to see so much difference between PBSO and Fire/Rescue, since most external salary surveys show rough parity between the two professions. (Note: in a later look at just sworn positions, the difference was not as stark.)

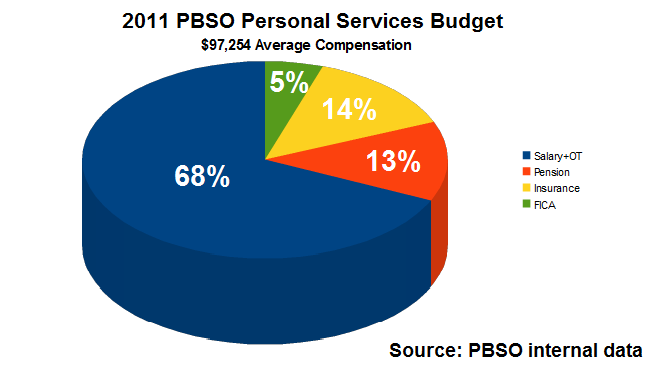

To illustrate the size of each benefit category, the following chart was assembled from information obtained from PBSO through an open records request.

A Word About Pensions

For the most part, county staff participate in FRS (Florida Retirement System) Pension plans. PBSO and Fire/Rescue do as well, but many are in the “special-risk” classes that are much more generous. The basic FRS plan allows full retirement at age 62 or with 30 years, with service credit of 1.6% for every year of service and a fixed 3% per year Cost of Living Allowance (COLA). The pension amount is calculated based on the “Average Final Compensation (AFC), the average of the 5 highest paid years, including overtime and bonus.

Special Risk classes get modified formulas. Firefighters for example, can retire at any age with 25 years of service, with a full 3% service credit for each year. To see how much more lucrative that is, consider the following example:

Two employees, one a county staffer another a Firefighter, both earn and average of $100,000 for their last 5 years, and each retires at age 62 with 30 years service. The firefighter’s pension is 88% higher than the staffer. Ten years later, at age 72, the firefighter is making 21% more than when he was working, while the staffer is only making 65% of their final pay. See table.

| Pension Class | AFC | Pension at retirement | Pension 10 years later |

|---|---|---|---|

| Normal | $100,000 | $48,000 | $64,508 |

| Special Risk | $100,000 | $90,000 | $120,952 |

It should be noted that Defined Benefit pensions are not widespread in the private sector, particularly for those hired in the last 10 or 15 years, and where they do exist, they do not feature cost of living adjustments, being in essence, fixed annuities. Comparisons of pension benefits are complex though, and we will leave that exercise to a future article.

External Comparison

To understand if these levels of compensation are within established norms, we looked for local statistics, starting with the federal government. The Bureau of Labor Statistics published its last survey of our area for May 2009, entitled “May 2009 Metropolitan and Nonmetropolitan Area Occupational Employment and Wage Estimates –

West Palm Beach-Boca Raton-Boynton Beach, FL Metropolitan Division“. The text of the survey can be found HERE

The sample includes about 510K employed persons who have an annual mean of $42,380 in May of 2009. To map against our three county groups, we extracted the averages for Fire Fighters ($62,110), Police and Sheriff Patrol Officers ($61,310), and their respective management groups. Since the county staff has a very wide range of job descriptions, some highly specialized, we didn’t think the category “Office and Administrative Support Occupations ($31,810) did it justice, so we used the overall county mean. For county management we used the category “Administrative Services Managers”. See the results in the following table:

| Area | BLS National Survey | BLS Local Area Survey | PBC Average from Salary Database | Number in group | Local Comparison | National Comparison |

|---|---|---|---|---|---|---|

| Sheriff Staff | $55,120 | $61,310 | $59,033 | 3278 | -3.7% | +7.1% |

| Sheriff Mgt. | $78,580 | $99,090 | $102,502 | 490 | +3.4% | +30.4% |

| Fire/R Staff | $47,220 | $62,110 | $71,840 | 1010 | +15.7% | +52.1% |

| Fire/R Mgt. | $71,680 | $94,600 | $111,284 | 494 | +17.6% | +55.3% |

| County Staff | N/A | $42,380 | $41,783 | 4994 | -1.4% | N/A |

| County Mgt. | $81,530 | $86,720 | $87,892 | 348 | +1.4% | +7.8% |

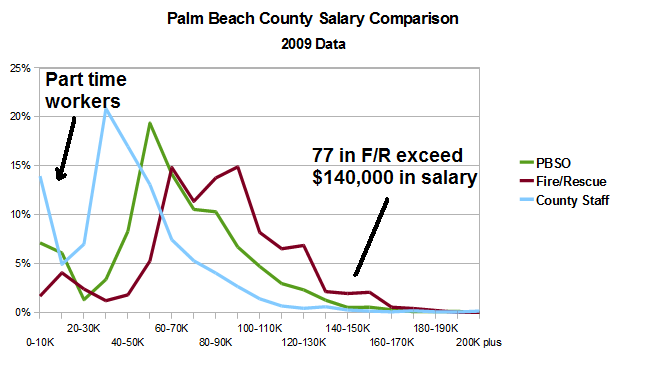

A Histogram showing the spread of salaries across our three groups looks like this:

To explain the very high averages for Fire Rescue we looked into the apparent excess of management. A database query on titles yields the following table. Note again that over a third of all employees have “supervisory” titles.

| Title Group | Number in Group | Average Gross |

|---|---|---|

| Chief | 51 | $146,414 |

| Captain | 268 | $116,909 |

| Lieutenant | 175 | $92,433 |

| Firefighter | 809 | $74,711 |

| Other | 201 | $60,285 |

Comparison of Sworn Titles

One criticism of the study has been that a comparison between Fire-Rescue and PBSO at the organization level does not take into account the relatively large number (43%) of civilian unsworn employees in the Sheriff’s office that earn less and are not in the “special risk” FRS class. To address the issue, we went back to the 2009 database and extracted the 2,111 sworn titles from PBSO (sergeant rank and above, plus protective services, Law Enforcement and Corrections). For Fire/Rescue, we used the 1303 titles of Lieutenant and above, plus Firefighter. Given that Fire/Rescue Captains and Lieutenants deploy with their equipment as field supervisors, we equated that group with PBSO sergeants, and considered them “first line supervisors” for comparison with the BLS data. Executive management (for which there is no separate BLS category) was counted as the 51 Fire/Rescue Chiefs (4% of sworn), versus the titles Chief, Colonel, Major, Captain, and Lieutenant in PBSO (6% of sworn). The results can be seen in the following table:

| Area | BLS National Survey | BLS Local Survey | PBC Mean | Number in group | Local Comparison | National Comparison |

|---|---|---|---|---|---|---|

| Sheriff Staff | $55,120 | $61,310 | $70,958 | 1742 | 15.7% | +28.7% |

| Sheriff Supv. | $78,580 | $99,090 | $100,961 | 242 | +1.9% | +28.5% |

| Sheriff Exec. | N/A | N/A | $124,754 | 127 | ||

| Fire/R Staff | $47,220 | $62,110 | $74,711 | 809 | +20.3% | +58.2% |

| Fire/R Supv. | $71,680 | $94,600 | $107,240 | 443 | +13.4% | +49.6% |

| Fire/R Exec. | N/A | N/A | $146,414 | 51 |

Using this criteria, the table shows that the sworn law enforcement and corrections professionals and first line supervisors at PBSO are paid at about a 29% premium to the national averages. This still pales in comparison to Fire / Rescue though, where Firefighters see a 58% premium and their supervisors about 50%. Executive management at Fire/Rescue gets a 17% advantage over PBSO.

Conclusions

From the foregoing data, we can draw some conclusions:

- County staff and average PBSO rank and file gross pay is just slightly more than the national average, and in line with the Palm Beach County urban area averages when measured on an organization-wide basis.

- PBSO management does quite a bit better than national average (+30%, both in aggregate and at the Sergeant level). This may possibly be justified by the fact that PBSO covers a large area and service population compared to peers, and likely is a more complex management challenge, although we did not have national data to compare. It is a premium that should be examined however.

- Fire Rescue gross pay greatly exceeds peer groups in the county, and are more than 50% ahead of national averages. This is pretty significant and needs to be thoroughly explained prior to the next contract negotiation.

- Although nationally (and in the county survey), police and fire agencies are paid about equally, PBC Fire/Rescue employees are compensated on average about 50% more than those in the Sheriff’s office, and their gross pay is 33% higher organization-wide (5-7% when comparing only sworn employees).

- Fire Rescue is extremely top-heavy. Over 33% of the entire organization holds the rank of Lieutenant or above. The span of control for Palm Beach County Fire/Rescue is therefore 2:1. That says every manager on average only supervises 2 people. By contrast, the span in PBSO is about 7:1 and in the county staff about 14:1. Fire-Rescue explains that each vehicle (fire or EMS, each with a crew of 3) deploys with a Lieutenant or Captain on board.

- FRS pensions for those not in high-risk classes are not excessive compared to private sector Defined Benefit plans (to the extent you can find them anymore), but the COLA is a feature that many private sector plans lack. For the special risk classes, the pensions are GOLD PLATED.

As taxpayers, we are pleased to note that Fire/Rescue is a modern, well-equipped organization that responds to emergencies with performance that is clearly satisfactory to the community. This service is very expensive however, and one wonders if the service is so much better than the national average that it deserves a 50% premium. We very much hope that the Board of County Commissioners will require a satisfactory answer to that question during the next contract negotiations.

Response from Fire-Rescue Chief Steve Jerauld

The following comments are offered regarding the document you provided:

- While some locales may do so, it has not been the County’s practice to look at law enforcement salaries and/or benefits when establishing compensation for Fire Rescue.

- That being said, any comparisons should be of like information. For example, the difference in the number of civilians employed by the two agencies can have an effect on the salary averages, and should be taken into consideration. Firefighting personnel work a 48 hour average work week, as compared to a typical 40 hour work week. We did not review your calculations, but it is not clear if 2011 budget figures are being used in a comparison to 2009 salary surveys.

- The conclusion regarding PBSO’s size and population served, which results in a more complex management challenge, likewise applies to PBCFR. We serve 1822 square miles from 54 work locations, including 18 cities and the unincorporated areas of the County.

- Regarding pensions, the benefits provided by the Florida Retirement System are not under the control of the County. Since it is a State system, the benefits are established by the Legislature.

- Number of Supervisory Personnel – Fire Rescue agencies deploy in a different manner than law enforcement. Fire Rescue units are frequently deployed to emergencies on a single unit basis, and as a result they are staffed with supervisory personnel. Fire Rescue maintains a Lieutenant on each Rescue unit, which in most cases is a 3 person crew. Each Engine or Aerial Company has a Captain assigned as part of the 3 person crew.

Steve Jerauld, Fire Chief

Palm Beach County Fire Rescue

TAB Legislative Wish List

- Modify the “PBSO Career Service Protection” Act

- Repeal the Fire/Rescue Sales Tax provision in FS 212.055

- Modify FRS to provide more flexibility

- Enact the “Local Government Accountability” bills (HB107/SB224)

Since its inception, TAB has focused on the spending side of the ledger, rather than taxes or other revenue, because the appropriations within the control of local officials are the levers on the “size of government” that we need to maintain the public/private sector balance.

A healthy local economy depends on a government that encourages and supports local business development, not one that creates disincentives through heavy taxation, stifles innovation through heavy regulation, or competes for employees and resources by using taxpayer dollars to overly compensate public employees.

When County Commissioners or others exceed the threshold of reasonableness on spending, we intend to firmly take them to task. There are instances though, where state statutes have tied the hands of local officials who are trying to do the right things. Many of these laws were passed at the urging of local special interests, such as the public employee unions, by legislators who they supported.

The County Government has a Legislative Affairs Department whose job it is to lobby for new laws and changes to existing laws that affect Palm Beach County. Each year they publish a “Legislative Issues” document that lays out the agenda.

In this year’s version, many of the items concern obtaining state funds for local projects. While many of these projects are desirable, we should not be treating state grants as “free money”. The test of any spending should be whether it is for an accepted public purpose, and whether it is affordable in the current economic climate. We also find items that support renewable energy standards, drilling bans and “climate change” legislation to be misguided, as are more subsidies for rail projects such as providing Amtrak protections on the FEC Corridor similar to the CSX indemnification for Sunrail.

That said, we find several items in this year’s agenda that we wholeheartedly support, and two that we oppose. Specifically:

FRS Reform

We STRONGLY SUPPORT the county’s proposed FRS reforms (Page 21), which:

- Require FRS participants to contribute to the plan

- Index by COLA rather than fixed increases

- Lengthen the re-hire time after DROP participation

- Offer incentives to voluntary moves to “investment option” plans (eg. 401K)

- Cap the number of overtime hours used in calculating “Average Final Compensation”

However, we feel the list of things to avoid are too limiting – all things should be on the table, including altering benefits for current employees (but not retirees), at least for future accruals, ending defined benefit plans for new hires and raising the retirement age.

Career Service Protection Amendments

We STRONGLY SUPPORT the county proposal to revise the “Palm Beach County Sheriff Career Service Legislation” (page 37). HB601 at the time of passage in 2004, this legislation essentially prevents any reduction in pay or benefits to most employees of PBSO, even during collective bargaining. It states:

“no existing employer-paid benefits and emoluments to all certified and non-certified employees of the Sheriff with regard to the pay plan, longevity plan, tuition-reimbursement plan, career-path program, health insurance, life insurance, and disability benefits may be reduced except in the case of exigent operation necessity.”

As we found out in the last round of budget talks, there can be no “exigent operation necessity” until the county has exhausted all its reserves and is essentially out of money. This means that neither the County Commission nor the Sheriff himself may reduce a benefit currently received or promised in the future, including the very lucrative PBSO longevity raise plan.

Fire/Rescue Surtax

We STRONGLY OPPOSE the county’s proposal to amend the changes brought by the “Emergency Fire Rescue Services and Facilities Surtax Act” (Page 32) so as to make it more workable and permit the return of the sales tax surcharge ballot initiative in 2012. TAB urges repeal of this act. Fire/Rescue should be required to justify its budget every year, just like any county agency, and not be funded by sales tax revenue with no oversight.

Floors for Library Grants

We also OPPOSE the county proposal to set funding floors for state library grants (page 33). All programs should be subject to adjustment in economic downturns. Mandatory funding floors, much like the provisions of the Career Service Protection Act, should not be enacted to prevent state or local governments from acting during times of fiscal challenge. It is hypocritical for the county to want to amend one and enact the other.

Local Government Accountability

Not on the county agenda, but on the TAB radar is a set of bills currently in committee (HB107/SB224 – Local Government Accountablility) that specifies (among other things) the amount of detail the Sheriff would be required to include in his annual budget proposal, specifically:

The sheriff shall furnish to the board of county commissioners or the budget commission, if there is a budget commission in the county, all relevant and pertinent information concerning expenditures made in previous fiscal years and to the proposed expenditures which the board or commission deems necessary, including expenditures at the subobject code level in accordance with the uniform accounting system prescribed by the Department of Financial Services. The board or commission may not amend, modify, increase, or reduce any expenditure at the subobject code level. The board or commission may not require confidential information concerning details of investigations which is exempt from the provisions of s.119.07(1).

Since transparency of the Sheriff’s budget is a Palm Beach County issue, we STRONGLY SUPPORT passage of these bills.

Tax Collector VOIP Project – Necessity or Re-inventing the Wheel?

During TAB’s initial look at the county spending, many people mentioned to us the apparent inefficient duplication of services that exists. Each of the Constitutional Officers, to varying degrees, manage their own infrastructure for things like Human Resources, Purchasing, and Information Technology. The arguments in favor of such an arrangement are sometimes compelling – such as the unique needs of the Sheriff. In other areas it is less clear that an established (and much larger) organization within the county structure could not do the job at lower cost and with better results.

This week, an example of further infrastructure divergence was brought to our attention. The Tax Collector, having assumed the responsibility for the county-wide motor vehicle offices from the state, has decided to upgrade the phone service within that function. Currently, Tax Collector network and telephone infrastructure is provided by county ISS.

Late last year, according to County ISS Director Steve Bordelon, ISS was asked to quote the work, and did so. It came as a surpise when they learned later that the Tax Collector had signed an agreement with an outside vendor (itpointe) for the purchase and installation of the new phone system in the Lantana and Palm Beach Gardens facilities, using a Cisco VOIP solution. ISS had previously adopted an Avaya solution (Cisco and Avaya are battling each other for dominance in the business communications market) and have over 1000 VOIP handsets installed throughout the county, a good track record of performance and reliability, and a trained staff ready to support the Avaya system 24×7.

When informed of this decision, Steve Bordelon wrote a memo to Jean-Luc Caous, the “Innovative Technology Captain” for the Tax Collector’s “Technovative Services” group (titles in the Tax Collector’s office are interesting – they even have a “Goddess of Excellence and Opportunity Leadership Centre”). In it, he explained the advantages of staying with the Avaya solution and further pointed out that the Cisco system cost of $49,041 compares to an equivalent cost of $30,822 for the Avaya, with the additional advantage of leveraging the existing VOIP infrastructure.

Additionally, he said this:

Proceeding with the installation of a Cisco VOIP telephone system will result in a duplication of resources and increased expenditure of taxpayer funds. Further, we are concerned that this decision could be a precursor to converting all of the remaining Tax Collector Offices to a separate phone system and perhaps, even a separate network, which would further increase the costs of government services to the taxpayers.

In his response, Mr. Caous said:

As part of transitioning the Driver’s License functions to the Tax Collector, the state advised us that we were responsible for obtaining the equipment and services required for our operations. As such, we have contracted with various vendors to implement solutions that are aligned with the organization’s strategies. We appreciate your recommendations that were put forward at our last meeting, however we feel that the CISCO VOIP solution better fits our requirements surrounding our new Driver’s License functions. Under our established project timeline, the PGA office is scheduled to be completed January 24th, 2011. Our office is too far along in the process at this point, and we do not want to deviate from the plan, which could jeopardize the project completion dates.

In addition, as mentioned in our previous discussion, the majority of the equipment to be installed would not be replicated. The new locations we are taking over require cabling work, switches, phones, etc., to bring them into our environment. These costs would have to be paid by taxpayers, regardless of whether the costs are paid by the state or the county.

Finally, it is not our intent to acquire a separate network but to leverage the county’s network infrastructure to run the technology that best meets our needs.

So is this decision in the interests of the taxpayer and the citizens of Palm Beach County? We called each of the memo-writers for their comments.

Steve Bordelon was gracious with his time, and explained some of the history of ISS support for the Constitutional officers and how it varies depending on who was elected to the post. He believes the decision is a mistake, but acknowledges that the Tax Collector is an independent entity and is free to make their own IT decisions. However Other Charter Counties in our peer group that he has studied (eg. Orange) make better use of centralized facilities.

Jean-Luc Caous declined to speak with us and instead referred the question to Tax Collector Anne Gannon herself. She told us that they will provide documentation that makes their case, but it will take some time to do so. She indicated that part of what drove the decision was difficulty working with ISS on the concept. On the goal to move to the VOIP system, they at first were told it could not be done in an off-site building, then that it would be too expensive. Finally, although asked to quote, ISS did not provide one to their satisfaction. The project was driven by the details of the handover from the state – the Tax Collector has signed a 50 year lease on the space in the state buildings, and acquired the computer equipment, but the phone systems were to be removed and used by the state elsewhere. Having to move quickly for a January 24 opening date, they bid the project to third party vendors and were satisfied with the price and capablilty of the vendor selected to provide the phones and connect them to the county system. ISS will do the cable installation. Ms. Gannon said she will provide further background on the project later and we agreed to report on it here.

In TAB’s view, the Constitutional’s operate through sub-optimization. Each makes their own decisions about what is best for their organization and proceeds accordingly, irrespective of the investments that have already been made in county infrastructure. (There are exceptions – Gary Nikolits contracts the development and operation of the EXCELLENT and specialized PAPA database system and the printing or TRIM notices to ISS).

There have not been strong incentives to do otherwise, and bureaucracies being what they are, people at all levels would rather control their own destiny by spending their budget dollars in a way that gives them the most control over their resources.

From a taxpayer perspective – this decision sounds like a bad deal – an example of “re-inventing the wheel”. Can Cisco and Avaya systems coexist on the same network? Probably, but it has been my experience (30 years in the IT business) that it is asking for trouble. Minor incompatiblities can result in finger pointing by vendor support staffs, particularly when a rivalry as fierce as Cisco/Avaya is involved. When that happens, support costs go up and reliablility goes down. It makes sense only in the scenario that the Tax Collector is planning to totally disconnect from the rest of the county and go her own way.

That said, it is clear that the working relationship between ISS and the Tax Collector’s office needs some work. While ISS thinks the decision is wrong and the solution too expensive, the Tax Collector believes they were not getting the service they required from ISS. Perhaps avoiding sub-optimization in the future requires mediation.

We think this is an excellent example of what needs to be discussed in the upcoming Charter Review. With the enormous fiscal challenges facing state and local governments this kind of thing is out of step. Many are making the case that the smaller Constitutional Offices should really be county dependent departments (and thus use county support services). While a case can be made for the independence of the Property Appraiser and Supervisor of elections (objectivity) and the Clerk (independent audit), the case for the Tax Collector was given as “not wanting the people sending the bill to also collect the money”. (The independence of the Sheriff is more complicated and will be addressed in a later post.) Perhaps there is a middleground that can provide independence, yet still have incentives to optimize common resources at the county level. Every little bit helps.

Fire/Rescue Sales Tax Surcharge to Make a Comeback

If you thought the Fire/Rescue Sales Tax surcharge was off the table, think again. Earlier this year, against significant opposition from the business and grassroots communities, the County Commission voted to place the measure on the ballot in 2010, only to withdraw it a day later on the advice of counsel. The stated reason was that the authorizing statute (which came into being primarily through the lobbying efforts of The Palm Beach Fire/Rescue Union) had significant flaws. The statute in question is Chapter 212.055 FS, Section 1 Subsection 8, entitled “EMERGENCY FIRE RESCUE SERVICES AND FACILITIES SURTAX”. This was added by SB1000 and HB365 of 2009.

In June, 33 of the 34 speakers were vehemently opposed to the measure and represented business groups, realtors, chambers of commerce, at least one city (the Mayor of Palm Beach spoke against it), grassroots

organizations, and political clubs. The lone voice speaking in favor simply delivered a statement from the Village of Wellington that they supported it. (Wellington is part of the county MSTU and is not one of the 12 municipalities that get a “vote” on the issue.)

The correct course in our view would be to REPEAL the statute– Fire/Rescue should have to justify its budget every year, just like other county departments, not have a multi-year slush fund in which to fund even more exorbitant compensation packages. (The AVERAGE compensation for Fire/Rescue employees under the current budget is $146,000 / year!).

The 2010 Legislative priorities of the current Commissioners however contains a line item “Fire Rescue Sales Tax Surcharge Glitch” on page 32. It says:

FIRE RESCUE SALES SURTAX GLITCH

During the 2009 Session, the Emergency Fire Rescue Services and Facilities Surtax Act was passed by the Legislature. In order to implement the provisions of the Act, several clarifications are needed. Support legislation that would provide the following changes to current law:

- The addition of a sentence that specifies that the term “emergency fire rescue services” as used in the surtax statute does not include volunteer fire department services.

- A statement that any surtax (all of which are subject to original approval by referendum) must be

reauthorized by referendum at least once every 10 years.- Clarification that a Municipal Services Taxing Unit is eligible to receive surtax proceeds under the

distribution formulas in the act.- Clarify provisions requiring that participating jurisdictions reduce either taxes or other revenues by

the amount of the surtax.- Include provisions that protect community redevelopment agencies from loss of revenue as

a result of imposition of the surtax.- Change in the date surtax collections will be initiated after approval from January 1 to October 1 to

ensure the surtax will not provide a windfall to participating governments.

Now is the time to contact your state representatives and ask them to REPEAL, not fix the Fire/Rescue surcharge addition to FS 212.055.

Commissioner Burdick Off to a Good Start

New County Commissioner Paulette Burdick is off to a promising start. TAB was impressed with her challenge to several Consent Agenda items at the December 7th meeting. Among them:

- She raised concerns with increasing fuel flowage fees at local airports, siding with the Aviation and Airports Advisory Board, which voted 4 to 3 against establishing the fees for the North County and Pahokee Airports and raising them at the Lantana Airport at its October 8, 2010 meeting. The other commissioners had no qualms about over-riding the board in search of revenue. They voted 6:1 for the fees with Ms. Burdick in sole opposition

- Ms. Burdick had an item moved to the 12/21 BCC meeting in order to explore local sources.

- She questioned the rationale for library warehouse leasing.

- She sought measurable performance standards in PBSO Law Enforcement Trust Fund (LETF) grants. Ms. Burdick noted that perhaps legislative relief was in order to allow these grants to be used in other circumstances, pointing out that the sums being considered could have otherwise been used for the Drug Farm or Eagle Academy if the statute were amended. Administrator Weisman deflected her questions to PBSO. (NOTE: For TAB’s view of the LETF, see below.)

- Most encouraging was Ms. Burdick’s opposition to the acceptance of a US Justice Department Community Oriented Policing Services (COPS), Hiring Program Grant award in the amount of $2,634,400 for the period of September 1, 2010, through August 31, 2013. While no matching funds are required during the grant period, there is a retention period of 12 months after the grant ends. The ongoing cost, assuming these ten officers are retained would be almost $1 million/year. The other Commissioners and Administrator Weisman expressed minimal concern – basically saying ‘what’s a million dollars in a four hundred million dollar plus budget?’ or ‘why worry about something 4 years down the road? Another grant will come up.’ The item was passed 6:1 with Commissioner Burdick opposed.

Kudos go to our newest Commissioner for considering the economy, the tax-payer and the long-term implications of ‘free money’. Keep it up!

NOTE: TAB considers the current operation of the LETF to be the Sheriff’s equivalent of the Commissioner’s “slush funds” from a few years back. The statute states clearly that the funds can only be spent on a narrow list of items, but PBSO spends the money on whatever they choose, with minimal justification. In September, the LETF was used to fund Cultural Council items that had been cut by the BCC. Today’s line item had funds for local charities. To see how much of a stretch this is – read the justifications: HERE

Florida Statute 932.7055 lists these as the only approved uses of LETF funds:

“… the support or operation of any drug treatment, drug abuse education, drug prevention, crime prevention, safe neighborhood, or school resource officer program(s). The local law enforcement agency has the discretion to determine which program(s) will receive the designated proceeds …”

Should Ethics Director Johnson Get a Raise?

A pay raise for the Ethics Director? This question has recently entered the public sphere.

Shortly after the Palm Beach County Ethics Commission was formed this year, Alan Johnson was hired in April as the Commission’s Executive Director. ( Press Release ) Mr. Johnson had been senior counsel for the Public Integrity Unit of the State Attorney’s Office.

At the time, the ethics ordinances had been in place for a few months, and discussion had already begun on the ballot initiative to bring the cities under the Ethics Commission’s jurisdiction, so it should be a surprise to no one that the measure passed and the scope of the Commission will be expanded, subject to the charter amendments that are to be written.

With expanded scope, larger budget and staff, Mr. Johnson has made it known that he would like a larger salary than the $118,000 plus benefits that was offered and accepted in April. Several Commissioners support this concept, suggesting that it was their plan all along. Commissioner Fiore went so far as to say they knew they were “underpaying” Johnson.

See the article on the subject by Andy Reid in the Sun Sentinel HERE

With the exception of the Fire/Rescue and PBSO employees who are compensated under a union contract, few if any county employees have had a raise in quite some time. Is it fair then to give Mr. Johnson a raise after only a few months on the job?

Let’s examine the facts.

In the database of county salaries (PBSO is excluded), Mr. Johnson’s $118,000 salary places him at number 328 in the total pay hierarchy when all county employees are considered. (Of course most of that list are firefighters – remember that their average compensation is currently about $140K. As a matter of fact, 69% of those earning more than Mr. Johnson are the 225 Captains and Chiefs and the like in Fire/Rescue). When only the county staff are considered, he would be number 103.

If PBSO were included in the comparison, there are an addtional 209 employees with total pay above $118K, so that would put Mr. Johnson at number 537 in the hierarchy.

Just above that level are the Assistant Director of Roads and Bridges, and the Assistant Director of Libraries. Just below that level is the Director of HCD and a title called “Fiscal Manager II”.

If you were to compare Mr. Johnson’s salary to the private sector, for an advise and consent, administrative job with 2 employees reporting to him, $118,000 is a lot. For the county though, where the compensation is plush and comfortable, maybe it is an outlier.

As a taxpayer, I believe that all the county salaries and benefits have reached levels that are unjustifiable and there should be a public outcry – particularly about Fire/Rescue. For Director Johnson though, I do believe he should make more than the Assistant Director of Libraries, and it is unfair to single him out for scrutiny when the rest of the county coasts by out of the public eye.

So yes – Alan Johnson should get a raise when the scope of the job expands to cover the cities. It would be premature for the Commission to act prior to that time however, since the job was offered and accepted at the current level, and the scope has not yet changed.

Volunteers Wanted for TAB “Shovel-Ready” Projects

As more volunteers come forward to work on TAB Research, and we have begun considering paid studies, the time has come for a “to do” list of projects that are “shovel ready”. The objective of these projects is to increase our understanding of the trends in county spending and taxation, and to bring to light areas of excess, or unsustainable trends that bode ill for the future.

Many of these projects can be undertaken purely from publicly available materials, others may require staff contact and/or public records requests. All will be useful as we make our case for a rollback of county spending to pre-boom levels.

If you would like to volunteer for any of these projects, or have more projects to add to the list, add a comment to the post or mail us at info@pbctab.org

If you decide to participate, you will not be working alone. The TAB team can provide the tools, technology, contacts, analysis techniques, and moral support. Join us today!

Project List

GB:General Budget

SS: School System

SO: PBSO

FR: Fire/Rescue

CS: Core Services

GS: Govt. Structure

CD: Capital/Debt

| Project Title | Tasks |

|---|---|

| GB1: Pension Cost Projection | Prepare a spreadsheet of the county pension costs by year since 2003, then project it 10 years into the future. List all the categories of pensions by type of position or bargaining unit, projecting them individually |

| GB2: Health Insurance Projection | Prepare a spreadsheet of the county employee health care costs by year since 2003, then project it 10 years into the future. List all the categories of plans by type of position or bargaining unit, projecting them individually |

| GB3: Peer County Comparisons | For the 5 largest Florida Counties (Palm Beach, Broward, Dade, Hillsborough, Orange), show the percentage budget growth (spending and ad-valorem taxes) for the years 2003-2011. In years that Palm Beach has exceeded the growth of the peer counties, examine which components grew the most (eg. PBSO, county staff, etc.) |

| GB4: Payers and Payees | Build a list of the municipalities and unincorporated areas of the county and for each, estimate their county tax burden (based on valuation). Based on population of each, determine per-capita tax burden. If possible, estimate “tax dollars returned” to those communities. |

| GB5: Allocation of ARRA Funds | Of the more than $500M in inter-govermental transfer funds, much in the last 2 years came from federal ARRA money. Track down where the money was spent and estimate whether it provided a general benefit to the county or was spent on special interests. |

| SS1: School Budget Trends | Develop a budget trend chart (spending and ad-valorem taxes) for the school system for the years 2003-2011, in a format for comparison with other county spending. |

| SS2: School System Salary Skew | Using a salary chart for all school system employees, analyze compensation for teachers versus administrators. Show growth in salaries for both groups from 2003-2011, as well as the number of teachers versus administrators. |

| SO1: PBSO Salary Skew | Using a salary chart for all PBSO employees, analyze compensation for sworn deputies versus civilian employees. Show growth in salaries for both groups from 2003-2011, as well as the number of each. |

| SO2: PBSO Spending History | Using information gleaned from pending open records requests, adjust the TAB PBSO trend data to reflect the population of the service areas by year, new jurisdictions added, and special mandates (eg. Homeland Security requirements). Build a chart of spending per capita (in the service area) and spending per call. |

| FR1: Fire Rescue Salary Skew | Using a salary chart for all Fire/Rescue employees, analyze compensation for union represented firefighters vesus other employees. Show growth in salaries for both groups from 2003-2011, as well as the number of each. |

| GS1: State Mandates | Build a list of Florida statutes that are impediments to substantive budget reduction in the county. Determine how much of the county budget growth can be attributed to state or federal mandates, and develop legislative proposals that could be used to restore local control. |

| CD1: Surplus Holdings | Develop a list of surplus buildings, land, and equipment (eg. Mecca Farms). Investigate the carrying costs and develop proposals for divesting assets to save money over the long term. |

| CS1: Appropriation Constituencies | Break down the county departments into “general benefit” (eg. parks, law enforcement) and “special benefit” (eg. Community Revitalization, Charity). Determine the size of the constituency of “special benefit” spending and examine the justification for that spending. |

| CS2: Program List | Build a list of all county programs and separate them into those that are clearly the function of government, those that are clearly not, and those in a gray area. Build a case to terminate the second category and create a plan to evaluate those in the gray area. |

Will Aaronson and Marcus run again?

Since the Broward term limits charter amendment has been trashed, what will happen in Palm Beach? If Judge Carol-Lisa Philipp’s ruling stands on appeal to the Fourth District, it will be controlling on our county as well.

So what will our two (currently) term-limited commissioners do? Burt Aaronson has not closed the door on a primary run against Anne Gannon in District 5. Karen Marcus on the other hand is in “wait and see” mode.

Chances are, if either of these incumbents is legally able to run and chooses to do so, the “power of incumbency” will make it very hard for a challenger to compete against them.

Read all about it in George Bennett’s Post article HERE.