Bob Weisman’s Response to TaxWatch Study

NOTE: The TaxWatch study was made available to commissioners and staff prior to their press release. This is the initial response from County Adminstrator Weisman.

From: Robert Weisman

Sent: Wednesday, September 07, 2011 9:01 AM

To: BCC-All Commissioners

Cc: Lisa DeLaRionda; John Wilson; Audrey Wolf; Ross Hering; Robert Weisman; Brad Merriman; Denise Nieman; George Webb; Joe Bergeron F.; Jon Van Arnam; Liz Bloeser; Shannon LaRocque; Steve Bordelon; Steve Jerauld; Verdenia Baker; Vince Bonvento

Subject: TaxWatch Report on Reserves and Property

You have been provided with a “draft” copy of a TaxWatch report on Palm Beach County that concentrates on our financial reserves and property. We have been able to give this only a cursory review since we were given access to it last night. The following are some brief comments in case you are asked about the report.

The financial reserve discussion appears very similar in opinion to the report that was issued 5 years ago. There does not appear to be anything in the reserve discussion that would affect our proposed budget. The funds they speak about are from multiple sources (impact fees, special revenues, bonds, general fund, etc) which are allocated to multiple projects. The only way funds could be made available to help balance the budget would be to eliminate and de-fund general fund projects that we have deemed necessary. We routinely examine project status and one of the ways we have balanced our budgets over the past few years is by taking money from completed or other projects whenever justifiable.

There would not appear to be anything new in the property portion of the report. Mecca is by far the largest asset we have, which it appears makes up 1/3 of the property they are talking about. The practicality and wisdom of selling our limited marketable property at this time is questionable. The numbers sound big, the reality is different.

We will evaluate and respond more fully after the final report is issued and we can review it in detail. If it discloses anything that can be useful in our budget balancing efforts, I can assure you that we will so inform you.

The 2012 TAB Proposal – September Update

The county has published their First Public Hearing package for the September 13 budget meeting. It presents a budget at the “rollback rate”, a 2.6% increase for the county-wide portion, generating $607M in ad-valorem revenue, and retains the current 2011 tax rate for Fire/Rescue and the Library System.

“Rollback rate” is a misleading term. While it is supposed to mean a rate that generates the same amount of tax revenue as the previous year, this one actually adds $4M to the county-wide tax burden. The 2.6% increase will likely understate the change to a homestead property held for some time, since the valuation may still not have caught up to the market value under the “Save our Homes” statute. Check the “TRIM Notice” that you should have received by now and look at the county tax line to see what it means to you.

Since Fire/Rescue and the Library system are not changing rates (and therefore collecting less revenue), the increase in county-wide taxes is offset by enough to hold the combined taxes to within $1M of the current budget. If adopted as proposed, this budget would collect a total of $835,144,556 in the 2012 fiscal year.

In July, the commission voted to set the “maximum millage” to the “rollback rate” of 4.8751. This means that in September they can adopt a lower rate but cannot exceed this maximum. Three of the four commissioners have indicated a desire to avoid raising the rates, and they could prevail. Therefore, to facilitate discussion, the budget proposal “bridges” the two rates by listing the programs that would have to be cut if the millage rate were kept at this year’s 4.75, but would be “restored” if the commissioners go with the higher “rollback rate”. Six separate proposals are provided, representing “steps” that add up to the $16.8M difference between the two rates (4.7500 vs. 4.8751). Controversial programs that are “restored” under the 4.8751 proposal include Palm Tran fares, lifeguard funding, nature centers, some financialy assisted agencies and about $12M in PBSO appropriations (less $5M in “excess fees”).

The first three points of our TAB proposal for this budget year are unchanged from July, but we have added a fourth point which reflects a conclusion drawn by Florida TaxWatch in their recently published study – namely that county fund balances are excessive compared to either our peer counties or objective measures of “prudent reserves”.

The TAB Proposal

- Maintain the county-wide millage at 4.75

- Take the majority of cuts from PBSO, not the county departments

- Take action to reduce the inventory of county property and reduce the debt

- Cover any remaining shortfall from current fund balances (reserves) which are excessive compared to peer counties.

We also want to see a charter amendment for a county version of “Smart Cap” placed on the 2012 ballot. Detailed arguments for each of these can be found later in this article.

Background

Last year, TAB was formed in July, after the county budget process was well underway.

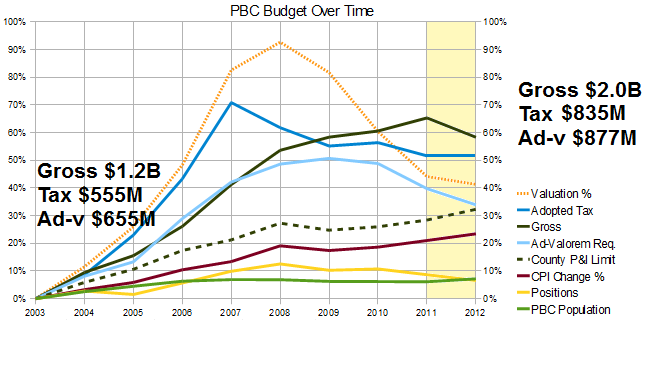

After researching the growth in county spending for the period 2003-2011, we concluded that it had grown 11 times the population growth and 3 times the rate of inflation. For FY2011, the proposed budget raised the millage by more than 9% on top of an increase of more than 15% in the previous year. Although the ad-valorem equivalent (and the total amount of collected taxes) declined in the 2011 fiscal year with the steep decline in property valuations, those with homestead properties saw their taxes go up.

Overall spending, propped up by state and federal stimulus funds, continued to increase in 2011 and only now is declining a bit. (See % changes from a 2003 baseline in the chart below). Adopted tax followed the valuation curve upwards until 2007 where after a slight decline as excessive reserves were burned off, it has been relatively flat, even as the economy has been in decline and valuations have plummeted. Ad-valorem equivalent (which is spending minus non ad-valorem revenue) has declined since 2010, while spending has been supported by intergovernmental grants.

With the weak economy and double digit unemployment in the county, we thought another tax rate increase was wrong, and argued for keeping the millage flat at 4.344. As part of the proposal, we went through the staff’s “green” and “blue” pages, and made specific spending cut proposals totalling over $50M, argued for deferring raises in Fire/Rescue and PBSO, and listed $100M in capital projects that could have been deferred.

In meetings with the individual commissioners, we made our case and had a productive dialogue, but were not persuasive enough to carry the day against the hordes of special interests (including PBA members supporting the Sheriff’s budget) that flooded the meetings and lobbied the commissioners to keep the taxpayer money flowing. The final budget passed with a 9.3% rate hike on a 4-2 vote, with commissioners Abrams and Santamaria voting against, and the district 2 seat vacant after the resignation of Jeff Koons.

This year we started earlier and have focused on educating community groups about the budget history, preparing them to join the discussion armed with the proper facts.

- The Sheriff submitted a budget request with spending that is 4% higher than last year, mostly to cover raises under the collective bargaining agreements in place until 9/2012. In the flat millage budget, he is being asked to cut 5% more than he saves with FRS, but so far has been unwilling cut any deeper.

- The property appraiser, who had been projecting a 6% decline in valuations this year, has softened his outlook to a 2.3% decline.

- FRS reform, passed by the legislature and signed by the Governor, will result in savings to the county departments, PBSO and Fire/Rescue of $15.4M, $20.6M, and $11.6M respectively (by our calculations). Note: The county shows the PBSO savings to be $18M.

- Although the difference between last year’s adopted tax ($603M) and the tax generated by flat millage this year ($591M) is only $12M, cuts are necessary because the “hole” is really $45M. This is explained (although not to our satisfaction) by “decrease in one time funding sources”, “increases in general fund transfers”, and other matters. See: County Budget Update – July 8

The following is an outline of the “TAB Proposal” for 2012:

The 2012 TAB Proposal

- Maintain the county-wide millage at 4.75

- County-wide property tax rates have risen 25.6% in the last two years alone

- Although the total taxes collected have declined over the same period, those with homestead properties saw double digit increase in their county taxes

- This year, the reduction in valuations has slowed from an expectation of -6% to a more modest -2.8%, reducing the pressure on the budget and millage rate

- TAB estimates that reforms to the Florida Retirement System (FRS), passed by the Legislature, will result in a $48M savings to the county this year ($20.6M in PBSO, $15.4 in county departments, and $11.6M in Fire/Rescue). This should be used to hold or reduce the millage, not for new spending on programs or salary increases.

- The county is still experiencing double digit unemployment and slow economic growth. This is not the time to be raising taxes.

- Thankfully, the Fire / Rescue and Library MSTUs are not projecting an increase in tax rate.

- Take the majority of cuts from PBSO, not the county departments

- County-wide ad-valorem taxes pay for the county departments and the constitutional officers, including the Sheriff. In the last 8 years, PBSO has grown from 46% of the budget to 58%.

- Most of the growth in the PBSO budget has been in personal services costs (salary and benefits), and PBSO deputies are now compensated more than 30% above the national average for similar positions.

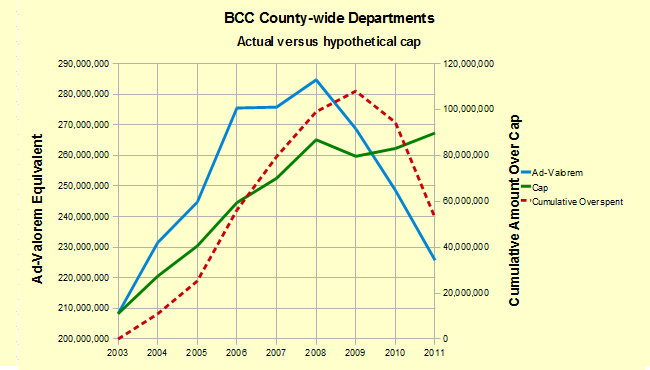

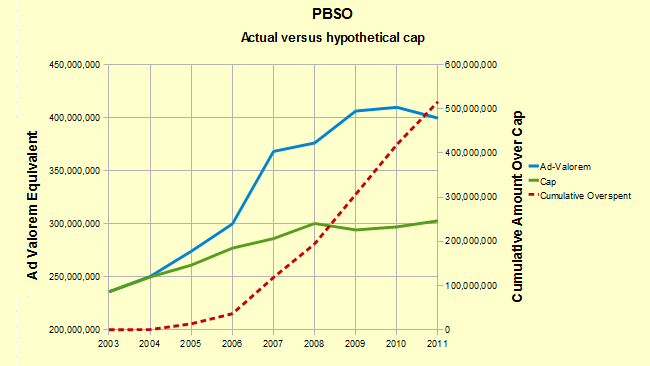

- Measured against a hypothetical population+inflation cap since 2003, county departments are now comfortably under the cap (although they exceeded it in the boom years by a cumulative amount of $50M). PBSO has greatly exceeded the cap in each year, with a cumulative overspending (versus the cap) of $500M in the 8 years. (See charts below)

- The Sheriff provides only the statutory minimum of budget data to the county (and the public) so it is difficult to see where the money is being spent. Through Chapter 119 (open records law) requests, TAB has determined that almost all the spending growth has been in salaries and benefits for employees covered by collective bargaining agreements, not in operating costs.

- The reduction to PBSO from $470M to $448M in the submitted budget would meet our criteria if allowed to stand.

- Take action to reduce the inventory of county property and reduce the debt

- Florida TaxWatch has conducted a Palm Beach County Study funded by the PBCA and others, that created an inventory of underutilized land and other property owned by the county, and compares our debt and capital programs to our peer counties. This study can be used as a blueprint for action to reduce the debt (currently $1600 per county resident with interest costs estimated at 14% of taxes collected) and make plans to sell off assets like Mecca Farms.

- The Clerk and Comptroller has identified the county-wide debt (including the Solid Waste Authority) as being significant already, and it is about to be increased even further with the building of the waste to energy facility and the convention center hotel.

- During the boom, windfall tax receipts were used to start projects that committed the county to long term debt that is difficult to justify now that the boom has ended. We need a plan to correct the problems caused by earlier bad decisions.

- TaxWatch obtained a list of vacant properties owned by the county and has assembled a table of current value. As long as these properties remain on the books it is a double liablility – there is a carrying cost associated with them and they are held off the tax rolls. Many of the over 2400 properties listed in the PAPA database as belonging to the county should be sold, even at a loss.

- Cover any remaining shortfall from current fund balances (reserves) which are excessive compared to peer counties

- The TaxWatch Study analyzed unreserved fund balances against peer counties as well as against an objective measure of “prudent reserves” for a government entity, even one within a hurricane zone.

- They concluded that the Palm Beach County fund balances are way in excess of what is needed and should be utilized to fund current spending until the balances fall at least below 40%.

- Sufficent fund balances exist in excess of a 40% cap to fund any shortfall this year and can be used in lieu of raising the tax rate.

It should be noted that items 3 and 4 can be used together. Property can be sold over the next 1-2 years and the proceeds can be used to replace fund balances used to fund current expenses. Asset sales can also be used to retire debt.

This year’s TAB Proposal is really not asking that much. With the smaller decline in valuations and the large savings from FRS reform, there should be very little difficulty in making the modest cuts that will be necessary to avoid an increase in the tax rates.

Smart Cap

Separate from the TAB Proposal for the FY2012 budget cycle, but important for long term budget restraint is a charter amendment to bring the state level “Smart Cap” proposal (SJR958) to the county. This will be a separate track, aligned with the charter review process, but if you agree with it, please mention it in the context of the budget discussion.

Adopt a “Smart Cap” charter amendment for county government

- The state-wide “Smart Cap” (SJR958) will be on the ballot in 2012. What is good for the state is good for the county.

- “Smart Cap” limits the revenue that can be collected to last year’s cap plus an adjustment factor that reflects inflation (change in Consumer Price Index) and population growth – an objective measure of “appropriate spending”.

- Although the decline in valuations has currently dampened the large increases in county spending that occurred during the boom, spending has continued to rise, even last year. When “normal” returns to the real estate market, a cap could prevent the out of control spending that occurred during the bubble.

- Unlike Colorado’s Taxpayer Bill of Rights (TABOR), a smart cap is based on last year’s cap, not on last year’s revenue. That prevents the “ratcheting down” of the cap that caused problems in that state during a recession.

- A well designed Smart Cap can provide emergency override (Supermajority BCC vote) and exemptions for unfunded mandates and other areas identified by the League of Cities as as problematic.

Growth in ad-valorem equivalents compared to hypothetical “Smart Cap”

Florida TaxWatch Report on County Reserves, Debt, and Property Utilization

At the request of the Palm Beach Civic Association, the Palm Beach County Taxpayer Action Board, and the Town of Palm Beach County Budget Task Force, Florida TaxWatch conducted a study of several aspects of Palm Beach County Finances.

In addition to an analysis of the county debt and reserves compared to our “peer” counties – Miami/Dade, Broward, Hillsborough and Orange, updated from their similar 2006 report, they also investigated the quantity and status of unneeded or underutilized property owned by the county.

The complete report is available HERE. What follows is a summary of the major findings.

Major Findings

1. County Fund Balance (“money in the bank”) is excessive

- The commonly accepted fund balance levels (unreserved) as a percent of expenditures for a government entity is 15%. Locally, 25% is considered prudent for hurricane preparedness. Palm Beach County has maintained a balance exceeding 50% over the last six years. Bringing this level down to even 40% would free up $188M of “excess reserves” that could be used for current spending, thus avoiding a tax rate increase through several cycles to come.

- Peer counties retain AAA bond rating with considerably less reserves

NOTE: This finding supports point 4 of the TAB Proposal – Cover any remaining shortfall from current fund balances (reserves) which are excessive compared to peer counties.

2. The County owns vast amounts of “Vacant” Property

- Of 2500 parcels owned, 353 parcels totaling 6200 acres are “vacant” – either unused or used for something other than their intended purpose

- Selling 25% of this vacant property would generate $54M in revenue and return $270K/year (unimproved) to the tax rolls

- Property record-keeping is unreliable and formal definitions and classification procedures are needed

NOTE: This finding supports point 3 of the TAB proposal – Take action to reduce the inventory of county property and reduce the debt.

3. County Office Space Allocation is overly generous

- Office size for executives and supervisors greatly exceeds state standards

- Reducing to standard could save $400K / year

In addition to these (and other findings), the TaxWatch team also made specific recommendations. Six were carried over from the 2006 study and are still relevant in 2011. The others are new and relate to the land and buildings aspects of the study.

Florida TaxWatch Recommendations

Recommendations from 2006 study that were not implemented:

- Establish a fixed cap on reserve funds as done elsewhere

- Implement a priority based budget process with performance metrics

- Adopt a budget reporting system that follows accepted standards and can be understood by the public

- Implement a Sunset Review process with automatic repealers

- Periodically rank all unstarted capital projects (partially implemented)

- Centralize services for constitutional officers

New Recommendations regarding property and buildings

Property

- Work with commercial realtor to plan and execute marketing plan to sell surplus properting over the next 18 months

- Institute formal definitions and procedures to identify “vacant”, “improved”, and “surplus” property

- Dispose of “strips” of land to adjacent property owners or bundle for sale

- Fully implement County Owned Real Estate (CORE) database and make available to the public

- Implement online marketplace to dispose of surplus property

- Apply full sunshine to property acquisition, exchange and sale process and separate from consent agenda

- Engage consultant to suggest utilization of surplus “right of way” property

- Incorporate vacant land disposition as part of County Comprehensive Plan

Buildings

- Require occupancy and vacancy rates of county assets be tracked

- Revise office space guidelines to align with Florida space allocation standards

- Make list of county owned buildings easily accessible to the public

Conclusion

TAB has argued that in this time of economic distress, tax hikes of any kind are counter productive. As the real estate bubble has deflated, the county has been increasing the tax rates in an attempt to prevent a decline in tax revenue. An alternative (in addition to the obvious – cut spending) is to buffer the shortfall with reserves accumulated during the “good” times. Not all government entities have that option as their reserves have been depleted.

The TaxWatch study points out that Palm Beach County is flush with reserves. Additionally, the county is carrying a significant quantity of unused or underutilized property that could be sold off over the next year or two, and the proceeds used to replace reserves spent to cover current spending.

It is our hope that the commissioners will agree and use this information to reject a tax rate increase for 2012.

September Budget Hearings – Some Background

At the end of September, the 2012 budget will be in place.

In spite of 4 years of decline in real estate values, the county keeps raising the tax rates to prevent any decline in tax revenue. If the private sector worked like government, all you would need to do to maintain your standard of living as a business owner would be to raise your prices. Everyone would have to pay it, whether they could afford it or not. Of course in the real world your customers would leave.

According to a national research group, tax-rates.org, Palm Beach County is in the top 8% of all the counties in the country for the tax on the median priced property. When measured compared to the median income in the county we are in the top 6%. It wasn’t always this way, but as the housing bubble inflated, local governments (including the county) collected more and more taxes, and now are trying to maintain that high level after the bubble has burst.

The total tax burden varies with the municipality (or unincorporated area) in which you live, but is typically about 2.2% of the value of your property each year when you include school taxes, municipal taxes, and a variety of special taxing districts. On top of that, there are non ad-valorem taxes on utilities, communications, gasoline, etc. It may be worse in New York or California, but few would say the taxes in Palm Beach County are low.

So what can you do about it?

First we have to stop the increases. The county commission voted 4-3 in July to set the “maximum millage” at “rollback”. This means the most that they can levy this year will collect about the same revenue as last year. Even though valuations have declined again, many properties are under water, and the county unemployment rate is in double digits, the county would like to continue collecting what it did last year.

TAB believes that county spending in some areas continues to be excessive, and the first step in turning things around is to refrain from raising the tax rate again this year.

The Legislature has done its part by passing pension reform, estimated to save the county between $26M and $35M depending on how you calculate it. Upwards pressure on costs though, including contracted pay raises for employees of the Sheriff’s Office make it hard to restrain the spending. It should be noted that during the time the county departments have trimmed back substantially, PBSO has not. The Sheriff’s budget now consumes 58% of the county-wide ad-valorem tax revenue, up from only 36% in 2003. Clearly that agency should be doing more to help the county balance their books at flat millage.

TAB proposes a plan with four actions:

- Maintain the county-wide millage at 4.75

- Take any further cuts from PBSO, not the county departments

- Take action to reduce the inventory of county property and reduce the debt

- Cover any remaining shortfall from current fund balances (reserves) which are excessive compared to peer counties.

The 9/13 meeting will be well attended by those who benefit from county programs and oppose any budget cuts. Typically, those who oppose tax increases are fewer and less vocal. You can help change the equation this year if you show up at the meeting and let the commissioners know you oppose a rate increase. TAB will provide specific arguments you can use on the website after we review the coming budget package. In the meantime, here are some references that may help prepare you to support the TAB proposal at the September 13 budget hearing:

- Higher Tax Rates in our Future – a synopsis of the July budget workshop

- County Budget Update – July 8 – Published prior to the July meeting and covering the origin of the $45M “budget hole”

- The TAB proposal and the County Budget – published in June prior to the first budget workshop

- Powerpoint Charts for the latest version of the TAB presentation

- Synopsis of last year’s budget hearings:

Fire Salaries Frozen in Martin County

Martin fire-rescue workers forgo raises in contract approved by County Commission

Tuesday, August 23, 2011

STUART — Martin County’s 300 fire-rescue workers will not receive raises in the next three years under a contract approved Tuesday by a divided County Commission.

That, combined with additional givebacks could total as much as $460,000 in savings.

Read the entire story by George Andreassi in TCPalm HERE

TAB Proposals for Charter Changes

Back in June, the County began public meetings about its ongoing Charter Review. The County Charter is its ‘constitution’ and describes Home Rule. There are 20 Home Rule or Charter Counties in Florida. Palm Beach County does not have a formalized Charter Review process, and this is the first comprehensive review to have taken place.

The Charter and the county’s charter review website can be found here. While there are a few changes that the Commissioners would like, citizens can input their own suggestions via the County Website. Suggestions are limited to 300 words per suggestion. Here is a link to the survey page. You can make as many submissions as you like.

There are many significant proposals that have surfaced, including county-wide commission districts, non-partisan elections, and converting some (or all) constitutional offices into county departments. We do not favor any of these as they appear to risk too many unintended consequences.

Attached are five proposals that we believe would improve county governance. One of these, “Smart Cap”, would have a direct affect on the county budget and we have explored that in depth in “Smart Cap – Good for the State, Good for the County”.

If you agree with any or all of these proposals, you can participate in the process by submitting the text contained within the box yourself using the county tool referenced above. To submit any of the ones listed below, just click on the [COPY] to the right of the suggestion you would like to copy, and then cut/paste from the text that comes up and submit that to the survey link above. All of the descriptions fall within the 300 word limit. Friday, August 26, is the last date on which submissions will be accepted on the county website.

Review all boards and advisory committees every four years

Objective: Formalizes a review process to remove unnecessary, redundant, or obsolete Boards and Advisory Committees.

Precedent and wording from Broward County Section 2.09 F

The County Commission shall adopt procedures to provide for the review of the performance of all Boards, Committees, Authorities and Agencies at least once every four (4) years. As part of its review of the respective Board, Committee, Authority or Agency, the County Commission shall determine, by resolution, that the applicable Board, Committee, Authority, or Agency is needed to serve the public interest, and the cost of its existence to the citizens and taxpayers is justified. The review provision shall not apply to any Board, Committee, Authority, or Agency established by this Charter.

County Version of Smartcap (this is a TAB proposal)

Objective: Limits spending growth to population growth and inflation formula

Reference: State Revenue Limitation (CS/SJR958). The yearly adjustment factor is calculated based on the previous year’s cap, not revenue collected. This avoids the problem encountered by Colorado “TABOR” which caused excessive reductions in spending during an economic downturn.

Precedent: Brevard 2.9.3.1(a): http://www.brevardcounty.us/countycharter/charter-article2.cfm – s29 and City of Jacksonville Sections 14.08/14.09: http://library.municode.com/index.aspx?clientID=12174&stateID=9&statename=Florida

Suggested wording: 1) For each budget year, county revenue collected is limited by the state computed adjustment factor defined in CS/SJR958. 2) Exemptions are allowed for unfunded mandates and certain other classifications of spending. 3) Emergency override is permitted with a super majority vote of the BCC.

Periodic Mandatory Review of the Charter by Independent Commission

Objective: Formalize the review of County Charter, instead of the ad hoc approach being taken during the current county review.

Precedent: 16 of the 20 Home Rule counties have a formal appointed* Charter Review Commission specified in their Charters. Period ranges from every 4 years to every 10 years. Size of Commission ranges from 10-15 individuals, with majority or 2/3 vote required to bring an amendment forward, and most scheduled to coincide with General Elections. *Sarasota County has an elected Charter Review Commission

Recommendation: Modify the charter to require a Formal review, by appointed review commission consisting of citizens, with an odd number of commissioners and majority vote, every 8 years, with results to coincide with a general election.

Debt Policy

Objective: Transparency and Accountability

Precedent: Charlotte County Sec 2.2.J

http://library.municode.com/index.aspx?clientID=10526&stateID=9&statename=Florida

Text from Charlotte County:

The county commission shall adopt and review annually, prior to April first of each year, a debt policy to guide the issuance and management of debt. The debt policy shall be integrated with other financial policies, operating and capital budgets. Adherence to a debt policy helps ensure that debt is issued and managed prudently in order to maintain a sound fiscal position and protect credit quality. Elements to be addressed in the debt policy shall include:

(1)The purposes for which debt may be issued.

(2)Legal debt limitations, or limitations established by policy (maximum amount of debt that should be outstanding at one time).

(3)The types of debt permitted to be issued and criteria for issuance of various types of debt.

(4)Structural features of debt (maturity, debt service structure).

(5)Credit objectives.

(6)Placement methods and procedures.

State of the County Quarterly/Annual Report

Objective: Transparency and Accountability by the administrative branch of the county

Precedent: Broward County 1.04 L: http://library.municode.com/index.aspx?clientID=10288&stateID=9&statename=Florida

Lee County: 2.3.A.1.(a): http://library.municode.com/index.aspx?nomobile=1&clientid=10131

The County Commission shall require and the public is entitled to have access to a Management Report published by the County Administrator, and made public on a quarterly basis, detailing the performance of the County government offices, divisions and departments. The Management Report shall include, but not be limited to, a report on the receipt and expenditure of County funds by each County office, division and department, and a report of the expected and actual performance* of the activities of each County office, division and department.

*Performance shall include measurements (benchmark metrics like head counts against peer counties) in key areas/contingent liabilities for long term union contracts and capital projects/annual market comparison of salaries and benefits (peer counties and private sector), other issues.

Little Progress in the IAFF Contract

The “negotiations” between Palm Beach County and the International Association of Fire Fighters, local 2928 have now been in progress for three months. With the exception of some minor cleanup in the text, there has been no agreement on anything. The major issues of starting salary (the county wants a 22% reduction) or employee contributions toward health insurance (3%) have not even been broached in the public meetings.

Seemingly minor issues, such as posting the seniority list on the intranet rather than on bulletin boards give rise to heated discussion, complete with implausible hypotheticals and the predictions of dire consequences. The county proposal to allow internal raters on promotional boards is treated by the union as if it was a wholesale rejection of a merit system for one of abject cronyism.

Yet with the exception of one heated exchange between attorneys over the “impasse” of qualifying overtime on a weekly rather than daily basis, the discussions have been cordial. The only problem is that they have accomplished absolutely nothing.

TAB volunteers have sat through these meetings, joined at various times by members of the press and a representative of the county Inspector General’s office. While the meetings have been about as exciting as watching paint dry, the way they have been conducted has been instructive in how public sector unions maintain their control over the functions of government.

Why this lack of progress?

The county, for their part, have proceeded in a workmanlike manner. Led by Attorney Robert L. Norton and Chief Steve Jerauld, their 6 member team has put their cards on the table in the form of detailed modifications to the existing contract document and walked through it in painstaking detail for the union representatives. They showed up for the meetings on time, and have been reasonable in the representation of their position. Of course their negotiating position is modest – other than the reduction in starting salary that affects nobody currently represented by the IAFF, there is no attempt to pare down the salaries and luxurious benefits enjoyed by current employees. The county team appears to be serious about completing the negotiations in a timely manner, and have tried multiple times to get additional meetings scheduled to expedite the process.

The union on the other hand, seems content to let the talks drift along. Led by Attorney Matthew J. Mierzwa, they have avoided agreeing to anything, even minor changes in wording. They showed up an hour late for the August session, a public meeting that had been on the county web calendar for quite a while, claiming “miscommunication”. (The county team was there on time, as were the observers). In the first meeting, halfway through the first “caucus”, they abruptly terminated the discussion and did not return until the next month’s meeting. One of their team of nine negotiators made the incredible statement that he had not read major sections of the county proposal because “he knew he wouldn’t agree with it”.

It appears to an outside observer that the county wants to conclude a new contract and the IAFF does not. Why would that be?

The contract expires at the end of September. The new county proposal contains new hire salary reductions, benefit cost sharing, and other things that disadvantage the union. The union version omits the reductions but does agree to forgo across the board salary increases in the new contract, subject to the condition: “Should the assessed value of properties in Palm Beach County or total revenues for Fire Rescue increase during the term of this agreement, the Union may reopen this Article for further negotiations.”

Maybe they want to run out the clock the way Congress does on major legislation. Perhaps they feel an improving economy will strengthen their hand. It is hard to say.

Although it is early to speculate, what if no agreement were to be reached? In that case, resolution would follow the rules of Florida Statutes Chapter 407.403 – “Resolution of Impasse” which involves mediation by a special magistrate. You may recall that this was a step in the resolution of the Fire/Rescue contract in the Town of Palm Beach. Ultimately it fell to the city council to impose what was a significant setback to the IAFF in that town. In this case, it would fall to the County Commission to impose a settlement.

The process continues in a planned all-day session on September 14, unless the proposal for four additional meetings requested by Mr. Norton is accepted. It should be pointed out that all participants in these discussions (6 for the county and 9 for the union) are being paid by the taxpayers. The attorneys of course are generating billable hours.

Two TAB Coalition Partners Organize Phonebank to oppose Tax Rate Increase

Is there really a swing vote who will decide if our tax rates are increased this year? It is possible.

During the July budget workshop, the vote to raise the maximum millage to rollback (4.8751) was 4-3. Commissioners Abrams, Marcus and Burdick voted no to the increase and all had good reasons to avoid a third hike in so many years. Commissioners Aaronson, Santamaria, and Taylor voted for the hike. They also gave reasons that are not likely to change in September.

Which leaves District 3 Commissioner Shelley Vana. Her votes on tax increases have been mixed, voting against the 14.9% hike in 2009 but supporting the 9.4% increase in 2010. This year, she voted to raise the maximum millage to keep “options open”, but suggested that there were more savings to be had and she would like to keep the tax rate unchanged when it comes up for the final vote in September.

After the July budget hearing, TAB sent the following in an email to Commissioner Vana:

It is not sufficient to say that it is a “starting point”. I’ve been watching this process for enough years to know how September will go. If you really think that another $12M (the difference between 2011 adopted tax and 2012 rollback) could be extracted from a $4B budget, and you intended to pursue it, then you would have voted for 4.75 to force the issue. For $12M you have poked a stick in the eye of the taxpayer. Actions speak louder than words.

If we are misreading your intentions, we would be glad to meet with you and correct our analysis.”

In response, and to her credit, she got in touch with us and made a convincing case that there was another $12M to be had and she just might “.. be the fourth vote ..” for flat millage in September.

We found this encouraging, but we also know that there are powerful interest groups in the county for continuing programs and taxes that speak very loudly to the commissioners. Those who do not want to see a tax rate increase are rarely heard. More to the point, it is the citizens of District 3 that should matter the most to the Commissioner, not any of the special interests, or even TAB.

Along these lines, two of TAB’s coalition partners have decided to reach out to the constituents of District 3 and educate them on the 2012 budget, and their Commissioner’s role as the potential “swing vote”.

The recently formed Palm Beach County Tea Party, with chapters in Jupiter, Wellington and Boca Raton will join forces with the South Florida 912 which meets in Palm Beach Gardens, Wellington and Lantana. Each of these groups is organizing a phone bank to contact District 3 citizens and ask them to make their wishes known to Commissioner Vana. They believe that many of the citizens would oppose a third year of tax rate hikes. If so, perhaps they can help the Commissioner find the additional $12M in cuts it will take to not raise our taxes again.

TAB applauds this effort and believes it is a new approach to broadening the county budget discussion beyond the commission chambers and the pages of the Palm Beach Post. It may turn out more attendees at the budget hearings who oppose another tax increase. At a minimum, it will have educated a larger group of county residents about the way their taxes are set.

If you would like to assist one of these organizations in their effort, you can contact them as follows:

Palm Beach County Tea Party: action@palmbeachcountyteaparty.org

South Florida 912: action@southflorida912.org

Fire / Rescue Contract Talks Continue

The July meeting of the negotiating teams for the 2012 IAFF contract did not move the ball very much, at least as far as we could see. As the meeting wrapped up, Chief Jerauld proposed holding additional sessions prior to the scheduled one on August 17 as there is a lot to do and little time to complete it.

More observers for the public attended this session, including TAB members, a reporter for the Palm Beach Post, and a representative of the Office of Inspector General. As this was anticipated, the county moved the meeting to a larger conference room at the Pike Road Headquarters.

The meeting consisted of much discussion of several draft agreements that had been prepared, and numerous “side agreements”, referenced by page number or paragraph position. None of the observers had copies of the referenced documents so it was difficult to follow. (We have asked for copies of all the materials prior to the next meeting). Much of the 3 hours were interrupted by “caucus time” when all the participants left the room for each side to confer among themselves – one of them 45 minutes in length. When we asked, it was explained that the referenced “side agreements” were contract modifications that were negotiated since the last contract was signed. None of these (or the current contract proposals) are available on the county website, but they are public documents which we will seek.

The major proposal by the county – reducing starting salary for new employees by 22%, was not discussed. It is our understanding that a counter-offer by the IAFF consists of an agreement for no raises for the next three years (subject to renegotiation if economic conditions improve), in return for retaining the existing starting salary of about $50K.

As described in Andrew Marra’s editorial “Cut these Alarming Salaries“, the problem is the existing salaries, which are approximately 50% higher than the national average and unaffordable in the long run without significant tax hikes or reduction in staff. Cutting the starting salaries would help, as would eliminating raises. If both were done, it may at some point bring Fire / Rescue Compensation down to earth. It would take a long time to do so however. There is nothing that we have heard in these current negotiations that will solve the problem near term, and choosing between starting salaries and wage freezes is a false choice. Both are needed, at a minimum.

We will continue to report on these negotiations as they progress.

Higher Tax Rates in our Future

On Monday, the county commission voted 4-3 to set the maximum millage at 4.8751, which would be a 2.6% increase over 2011. Maximum millage is the number that may not be exceeded when public hearings on the budget resume on September 13.

Following back-to-back increases totaling over 25% in the last 2 years, the commissioners had directed staff in February to create a budget that did not include a tax increase. This would have resulted in $12M less tax revenue collected because of still declining property values, but was offset by cost savings of $25M from reform of the Florida Retirement System (FRS) by the legislature. Other factors however, including reduced interest income and fund balance issues, resulted in a shortfall estimated at $40M and led to a proposal of cuts to popular programs.

Commissioner Aaronson, who is known for ongoing support for raising taxes on others to pay for services in his district, assured us that “it is only a starting point”.

Like Groundhog Day (the movie), the budget discussion plays out in a similar fashion year after year. A low or minimal rate increase is presented, combined with cuts sure to bring out the supporters (Palm Tran Connection, Nature Centers, Financially Assisted Agencies). A “reasonable alternative” that raises tax rates “just a little” for “pennies a day” is offered by Administrator Weisman, and after several hours of public comment, mostly by beneficiaries of those programs, the commissioners vote in July to set the “maximum millage” to the larger figure. Then, in September, after 8 weeks of “trying” to find additional savings, the commissioners decide they have no choice but to adopt the maximum as the final tax rate. Then the cycle begins again. Any guess as to how this will end this year?

To their credit, Commissioners Marcus, Abrams and Burdick voted against the higher tax rate. Paulette Burdick, in her first budget season as a commissioner, attempted to actually set priorities – facing down PBSO CIO George Forman over further cuts to the Sheriff’s budget, yet supporting continued funding for the financially assisted agencies.

Accepting the higher rate were commissioners Aaronson (no surprise), Taylor (who didn’t think 2.6% was significant), and Santamaria. None of these were surprises as they had made no moves toward the lower rate in the June workshop.

The more curious vote was by Shelley Vana, who at first seemed to be seeking additional savings (efficiency, etc) to prevent the tax hike, but voted for it anyway. Like Aaronson, she said it was a starting point and they can “try” to find additional savings before the September sessions. Actions speak louder than words commissioner. Don’t expect any credit for rhetoric.

From a TAB perspective, those of us who spoke against the tax hike were outnumbered by those seeking program dollars. While it is difficult to get working people to attend a morning meeting, we hope those of you who did not attend were able to send email or other communication to let your voice be heard.

Those who did speak for the lower tax rate, included Jack Borland, Francisco Rodriguez, Mel Grossman, Pam Wohlschlegel, Carol Hurst, Victoria Thiel, Dionna Hall, and Fred and Iris Scheibl.

For the next 8 weeks, TAB will be refining the argument against the higher rate and attempting to increase citizen awareness and involvement in the budget process.